PAYBACK: When money presents you with a mirror!

Hosted loyalty programs in their combination with bonus points, personal identification cum payment cards and multichannel marketing platforms are quite a common feature in contemporary consumer experience. Almost everywhere cashiers keep strenuously reminding you to scan your personal loyalty card (let this be PAYBACK, Deutschlandcard, Plenti or any other). And each time you do, you’re selling some of your personal data for bonus-points, coupons and miles.

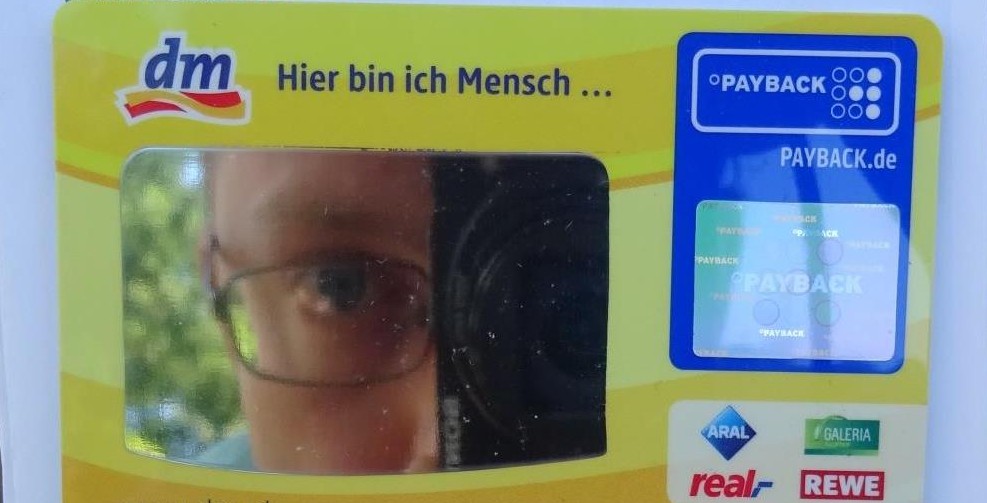

My first PAYBACK card (see image) came with a mirror and, well, I was immediately fascinated by such a profound feature. Somewhat naively, perhaps, I thought of this as a strong, farsighted and purposeful symbol. According to my immediate association the mirror represented the potential revolution that new connections of personal identity with money, payment and information may bring along.

Looking into the mirror of my brand new loyalty card I felt it wanted to tell me something. Perhaps like that:

“Hey, welcome to capitalism 4.0! I am your personal loyalty card – and I shall be watching you! From now on you are an esteemed member of our growing community. Look at how I reward you with points for every purchase you make and for all the faithfulness you show us as a customer. It’s your money which you spend, and it is also for your convenience that I can store and process all the data your transactions create. I can send you personalized ads and I’ll help to create some valuable benefits for you – I mean those kinds of information and those kinds of products that you really want to have. From now on I’ll develop the capacity of keeping track with your transactions. Therefore, always keep in mind that what I value is you! I’ll just be the mirror of your moneyness!”

However, part of my fascination rested on a simple confusion: It turned out that the card with the mirror was not “the” PAYBACK card, but only one of many different cards whose designs simply vary with the retail-brand you get it from. I got my card from DM – the biggest European drugstore chain and one of the early on partners of PAYBACK. To my quick disappointment the mirror did not have a deeper meaning at all – it was just a minor marketing gimmick, a symbol at best for the body care products that DM sells.

—

Nevertheless, let me add a few reflections:

Plastic cards of all kinds are a relatively new incarnation of money, and I should immediately add that they are still a rather interim form in a far more radical move from cash to digital payment. In stark contrast to cash, however, plastic cards are personalized devices which authorize and record transactions between accounts (often though not always via the institution of credit). Transactions are digital but therefore “plastic money” conveys information, generates data, and entangles its issuer and users in a traceable relationship. In this way plastic money creates a “new sociability … with far reaching implications for actors at both macro and micro (household) levels” (Guseva and Rona-Tas 2017: 202-203). While this does certainly not only open “enormous possibilities for surveillance and social control” (Ibid. 203) but also new ways of personal participation where monetary transactions could become a way of self-expression and of keeping track with complex networks that we each generate (Hart 2009: 101-102), it seems nevertheless true that the use of plastic money raises the stakes for those who are in control of the intelligence which transactions generate in sum (see Guseva and Rona-Tas 2017).

The rise of hosted loyalty programs such as PAYBACK, Deutschlandcard, Plenti etc. is just one among many related developments. Moreover, there is a great variability of how these hosts use personalized cards to combine money, payment and the collection of data. However their common feature is that customers are rewarded with bonus-points, miles or coupons – i.e. a “special currency” (I may soon write a related post) which is valid only within a limited sphere of participating brands and retailers. Based on this feature your personal loyalty card can, for example, come with or without the additional function of a credit card (in the case of PAYBACK this is Visa or American Express) while the issuer may also reward you with further incentives in bonus points or discounts whenever you make use of it. Yet, independent of how you choose to pay (i.e. whether you use cash, credit or debit cards), the deal is that if you want to receive bonus points at all, you need to scan your card along with every purchase you make. The points are stored on your personal account and can be redeemed like money as long as you use it within the allowed “sphere of exchange” (regarding the anthropological concept of “spheres of exchange”, see Röschenthaler 2010; cf. Bohannan 1955).

However, back to my original confusion: I have no clue whether or not PAYBACK and similar companies think broad enough about the institutions and technologies they create and, more importantly, with what kind of morality or philosophy their managements envision and weigh the possibilities, powers, responsibilities, dangers and benefits that may ensue from the fusion of payment with personal data, producer-consumer communality and the issuance of special currencies like bonus points. Certainly they are pioneers in a new age of money.

Yet, compared with the excitement I felt when reflecting myself (and the topic of plastic money) for the first time in the mirror of my brand new loyalty card, I feel a bit sobered. I’m still fascinated when I think about the possibilities. Looking into the mirror of my DM-PAYBACK card, I still see a reflection of myself – and well, it continues to have some appeal ;)! But by now it rather reminds me how someone else attempts to seize my personality – bribing me, quite successfully indeed, with marginal bonus points into an agreement of selling my data (i.e. who I am, but far more importantly where, when and what I purchased, how I paid, how much I spent, how I react to offers and incentives). Put facination aside, I have little doubt that the data is used in the creation of a system which, unlike the mirror, doesn’t necessarily want to value my priceless personality but creates value from understanding and manipulating my behaviour.

Actually this does not yet seem much like a revolution – it’s still the kind of antiquated economic-cum-bureaucratic ideology that values anonymity in that it converts persons into figures in order to gain a degree of control over masses; squeezing out some short-sighted profit while obscuring and disrupting the new sociality and mutual responsibility that could otherwise emerge (see also Guseva and Rona-Tas 2017: 203). It remains a worthwhile discussion (see Spickerman et al. 2015) whether the tracks and traces of data I leave belongs to the free commons, whether it is private property that can be claimed, protected and sold or whether it is perhaps best understood as both a shared social capital and a personal currency. Yet what I really lack – if only for the purpose of self-reflection – is access to the data I help to generate and of which I am a part. And here it may also be worth remarking that while all the knowledge concentrates increasingly in the hands of just but a powerful few this is in perfect symbiosis with laws governing data protection and data security (i.e. laws that deny access to everyone else).

—

Mirror, mirror on the card, who is the smartest in the art?

There are indeed some minor tendencies worth mentioning: PAYBACK for example offers the option of re-converting the bonus points at the checkout counter (at the current rate of 1 PAYBACK point = 1 eurocent). They also offer the opportunity to donate points for a good cause. It is also true that, when I login to my PAYBACK account, I can see a record of how much I spent each time I visited a particular merchant. Nevertheless, wouldn’t it be great to pay back a little more? I mean more than a very meagre share in bonus points which are tempting like money, yet are anything but a substantial reward! I sure want more than breadcrumbs of the long term intelligence I help to create!

How, for example, about providing me with a more detailed record of what exactly I bought – perhaps with the feature of categorizing my expenses; of comparing the latter with general averages; of ranking them according to the bargain I made or (perhaps more worthwhile) according to their sustainability in the production chain? How, perhaps, about allowing me to make certain results public – for example in order to show to others how responsible I am as a consumer; or how much bonus points I donated and for which cause? How about rewarding me with bonus points, not only when I buy, but when I participate – say in polls, for example about the company’s future orientation, its aims, philosophies, visions and values – like a true stakeholder? Or perhaps (though dangerous indeed) when I act according to such collectively identified aims? No less important, how about showing me how the collected data is really used, how it leads to improvements, and how loyalty means that “we” become better than other players – be it in the field of shopping experience, or with regard to alterations in the product portfolio, the just mentioned production chain, or the creation of new brands, new flows of information and new forms of sociability among producers, retailers and customers?

In short, how about sharing the intelligence; making me an active participant rather than a gregarious animal? A true member of the community rather than a passive producer of the data which (possibly) can be used to manipulate what I do? Certainly I would become more generous and more comfortable with providing information about myself – if I only had the same kind of access; if I was really able to collaborate. I wonder whether it could be much more profitable – even for the hosts – to offer ways of making the institution of money, payment and commerce, how it generates big data and whatever this produces, a bit more social, more democratic, more responsible, and more valuable! Certainly this would have a true impact upon loyalty and in this way it would raise collective stakes. Perhaps all this is just in the making. Perhaps the entire model will soon be overhauled by the blockchain. But how can I dare to trust? Dear marketeers who provide me with a loyalty card that comes with a mirror: One thing I’d love about loyalty, if I were sure to see the value!

—

References

Bohannan, Paul. 1955. “Some Principles of Exchange and Investment among the Tiv.” American Anthropologist 57 (1): 60-70.

Guseva, Alya and Akos Rona-Tas. 2017. “Money talks, plastic money tattles: the new sociability of money.” In Nina Bandelj, Frederick F. Wherry and Viviana Zelizer (eds.), Money talks: explaining how money really works. Princeton and Oxford: Princeton University Press, pp 201-214.

Hart, Keith. 2009. “Money in the making of world society.” In: Hann, Chris und Keith Hart (eds.), Market and society: the great transformation today. Cambridge: Cambridge University Press, pp 91-105.

Röschenthaler, Ute. 2010. “Tauschsphären: Geschichte und Bedeutung eines wirtschaftsethnologischen Konzepts.” Anthropos, 105 (1): 157-177.

Spiekermann, Sarah, Rainer Böhme, Alessandro Acquisti, and Kai-Lung Hui. 2015. The Challenges of Personal data markets and Privacy. In: Electronic Markets 25(2): 91–93.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Honestly I just hate it when I get asked for my payback card + not fascinated but terrified by such development! Still, your site is great. Pl. Keep on going!

Yes it’s all a bit frightening, and most of it is simply annoying. However I believe that while payback and co are developing powerful technologies the degree of how conciously customers participate in this process will make a huge difference.

Best, jens